I’ve been thinking about this a lot lately after coming across a cluster of startups trying to upend market research using AI. Within the span of the last couple months, companies like Simile and Aaru have raised hundreds of millions of dollars chasing the same idea: replace traditional consumer research with AI-generated simulations. It caught my attention because it cuts right to a problem I’ve run into throughout my career in BD. One of the harder parts of business development and partnerships is figuring out how customers will respond to something before you’ve built it. Will they actually want this product? Will they adopt this feature? Will the new product/service cannibalize other areas of your business? These questions typically sit at the center of most BD decisions and yet we often have to answer them with surprisingly limited information using more “gut” instinct.

Category: Venture Capital

Update (March 2026)

As I alluded to in my post below from just two months ago, ChatGPT has scaled back their Instant Checkout product given a less than ideal customer experience and has opted for fewer more end-to-end integrations which was my recommendation. Walmart, for example, saw ChatGPT checkout convert 3x worse than Walmart’s own website.

_______

A bit of a longer post today given all the platform deals that have been taking place (Waymo partnering with Uber, ChatGPT rolling out services from booking hotels to buying physical items, etc), that I wanted to share my experience having done these types of deals along with key learnings.

I’ve been reading daily, both articles and through posts on LinkedIn, about OpenAI enabling new services via ChatGPT, everything from being able to get an Uber, to book a reservation at a restaurant to ordering groceries via Instacart. None of this is surprising since when OpenAI launched ChatGPT plugins (and later custom GPT apps), they weren’t shy about the ambition. Sam Altman effectively hinted at an “App Store for AI” being a future where you could order a rideshare, book a table, or grocery shop all through ChatGPT’s interface, without ever touching a separate app. The idea, in theory, would be an AI App Store that would unify countless services behind one conversational interface (ChatGPT), sparing us the jumble of apps on our phones. In practice, however, the execution to-date feels like its fallen short ultimately because OpenAI’s strategy emphasized breadth over depth, integrating dozens of partners quickly, at the expense of building truly seamless experiences for the end user. The result is mostly a collection of clunky, half-baked plugin interactions that feel more akin to affiliate marketing than a truly end-to-end integration.

Every new platform faces a classic dilemma whether to go broad fast or go deep on a few core use cases. Google went deep for example with products like Google Maps enabling only affiliate type links for 3rd party partners. OpenAI clearly chose to go broad, opening a wide range of ChatGPT plugins in months. Unfortunately, many of these integrations lack the tight product coupling needed to make them useful. The user experience feels disjointed. This isn’t a new problem. I’ve seen the pitfalls of “breadth over depth” play out before, across various partnership bets in tech. In fact, five firsthand partnership anecdotes from my career illustrate why shallow integrations underwhelm, and why deep, end-to-end integrations are what truly drives the best experience for the customer. Each story, from ride-hailing to meal kits, carries a lesson that OpenAI (or other platforms) would do well to heed.

AI is moving fast, but the business models behind it are even harder to decode. I’ve been spending time mapping out who the key customers are and how money flows through the system. Foundational providers (OpenAI, Anthropic, etc), wrappers (Harvey, Jasper, etc) — each plays a different role in the value chain, and investors and operators alike are still figuring out how to navigate the commercial landscape.

I’ve built and scaled growth models at companies like Newell Brands, Casper, Blue Apron, and Lime, and today I advise startups, investors, and corporates on how to navigate this shifting landscape. To cut through the noise, I created this AI Business Model Guide — a simple framework to understand where opportunities lie and where risks emerge.

If you’re building in AI or exploring partnerships, this guide is a starting point. The presentation is embedded below.

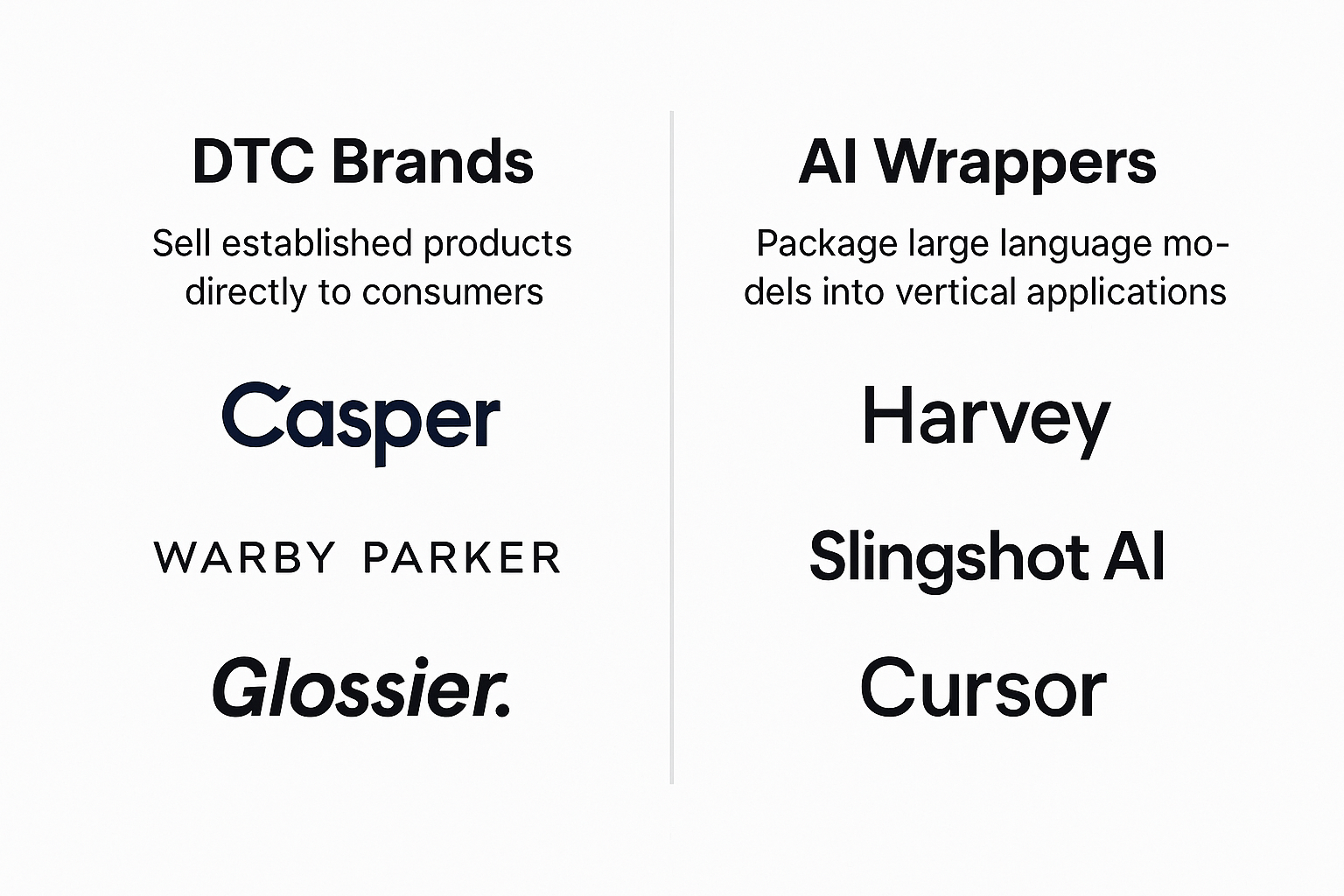

Over the last year, niche AI startups have exploded onto the scene. Companies like Slingshot (mental health), Harvey (legal), and Jasper (marketing), Cursor (code editor) are racing to stake out territory on top of large language models like ChatGPT and Gemini. At first glance, they feel innovative and differentiated. But if you squint, they look a lot like the early wave of direct-to-consumer (DTC) brands — Casper, Warby Parker, Glossier, Harry’s and Peloton — that disrupted incumbents not by reinventing the product, but by reshaping the story, distribution, and consumer experience.

I saw this firsthand at Casper. We weren’t reinventing the mattress — foam was foam — but we were reinventing the consumer experience and telling a story incumbents weren’t telling. We addressed a lot of the pain points in the legacy purchase experience (returns, trial, etc) with novel solutions.

The analogy here is hard to ignore.

If you have a small but growing business selling on Amazon or even direct-to-consumer (D2C) you’re bound to hit a point where you require money to scale. For as much as the media talks about venture capital, the reality is that less than 1% of startups here in the US are able to raise money from VC’s. The challenge, however, is that consumer brands often have working capital needs associated with carrying inventory or affording increasingly expensive paid media. So where do these types of businesses get the cash to grow? Traditional lenders, such as banks, often have strict covenants in their terms and have not historically catered their products to this cohort, but a growing number of new, innovative solutions are disrupting the model. I should note that pre-revenue/pre-product startups are likely not going to be a candidate for institutional debt – but a convertible note, SAFE or crowdfunding remain a viable alternative at this early stage. As a side note on crowdfunding, the SEC recently increased the cap for fundraising via this channel to $5m (from $1m) which I suspect will open up more activity in this space.

If you have a startup and you’re venture backed, then you ultimately need an exit. Historically, this has been through M&A or by going public. However, with the exception of some SaaS deals, there’s not been a lot of M&A activity recently in the consumer space. Strategic buyers often feel many startups are overvalued and aren’t interested in paying the premiums. The alternative is an IPO and there’s a lot of new innovation to look forward to here. Earlier this year, there was growing support for direct listings among some high profile VC’s, namely Bill Gurley, who felt many startups were leaving “money on the table” by going through a traditional IPO. Slack and Spotify are two examples of companies that have done direct listings. His argument is that in a traditional IPO the bankers engineer the deal to get a pop for their institutional clients and ultimately the company doesn’t get to keep any of the upside. Case in point is Snowflake (SNOW) that went public yesterday via a traditional listing. The stock jumped 111% on the first day and as a result left $3.8b on the table. The downside with doing a direct listing has been the inability to raise capital as has been the case in a traditional IPO. That said, the NYSE has been working with the SEC on a way to do a primary raise concurrently with a direct listing that was recently approved but has since been rescinded as other parties pushed back. More to come here.

This is a period of immense uncertainty but also a time for great opportunity. Some of the most well known companies were created during past periods of volatility. Apple and Microsoft were born during the OPEC induced recession of the 1970’s. Netflix survived the Dot.com bubble and came out stronger than ever, and Airbnb was born during the 2007-2008 recession. Fast forward to today and there seems to be two schools of thought on investing during the current Covid-19 pandemic. Either it’s batten down the hatches and conserve cash or let’s use this as an opportunity to double down on our winners and also invest in other startups that are booming due to stay at home restrictions. As we’ve seen in the public markets there are multiple bulls out there in certain sectors and the same theme applies to venture.

Venture capitalist Marc Andreessen coined the term “Software is eating the world” nearly 10 years ago. His argument that software would be at the heart of every business moving forward could not have been more astute. For example, Amazon’s not a retailer; their primary capability is their software technology enabling sellers around the world to get their products to consumers. The same could be said for their AWS cloud business; again a software play. Uber, Google, Facebook, Netflix, and to some extent Apple’s app store business, are all examples of companies that are fundamentally software first. Interestingly, this same software has empowered a foundational shift in business model. It has enabled disintermediation. The complex network of intermediaries that have existed historically have been circumvented which has led to the world of everything being direct-to-consumer (D2C) or direct to source. Many think of D2C as mainly having an impact on consumer goods, but the theme permeates into numerous industries. Here are some examples: