I’ve been thinking about this a lot lately after coming across a cluster of startups trying to upend market research using AI. Within the span of the last couple months, companies like Simile and Aaru have raised hundreds of millions of dollars chasing the same idea: replace traditional consumer research with AI-generated simulations. It caught my attention because it cuts right to a problem I’ve run into throughout my career in BD. One of the harder parts of business development and partnerships is figuring out how customers will respond to something before you’ve built it. Will they actually want this product? Will they adopt this feature? Will the new product/service cannibalize other areas of your business? These questions typically sit at the center of most BD decisions and yet we often have to answer them with surprisingly limited information using more “gut” instinct.

Category: Startups

Update (March 2026)

As I alluded to in my post below from just two months ago, ChatGPT has scaled back their Instant Checkout product given a less than ideal customer experience and has opted for fewer more end-to-end integrations which was my recommendation. Walmart, for example, saw ChatGPT checkout convert 3x worse than Walmart’s own website.

_______

A bit of a longer post today given all the platform deals that have been taking place (Waymo partnering with Uber, ChatGPT rolling out services from booking hotels to buying physical items, etc), that I wanted to share my experience having done these types of deals along with key learnings.

I’ve been reading daily, both articles and through posts on LinkedIn, about OpenAI enabling new services via ChatGPT, everything from being able to get an Uber, to book a reservation at a restaurant to ordering groceries via Instacart. None of this is surprising since when OpenAI launched ChatGPT plugins (and later custom GPT apps), they weren’t shy about the ambition. Sam Altman effectively hinted at an “App Store for AI” being a future where you could order a rideshare, book a table, or grocery shop all through ChatGPT’s interface, without ever touching a separate app. The idea, in theory, would be an AI App Store that would unify countless services behind one conversational interface (ChatGPT), sparing us the jumble of apps on our phones. In practice, however, the execution to-date feels like its fallen short ultimately because OpenAI’s strategy emphasized breadth over depth, integrating dozens of partners quickly, at the expense of building truly seamless experiences for the end user. The result is mostly a collection of clunky, half-baked plugin interactions that feel more akin to affiliate marketing than a truly end-to-end integration.

Every new platform faces a classic dilemma whether to go broad fast or go deep on a few core use cases. Google went deep for example with products like Google Maps enabling only affiliate type links for 3rd party partners. OpenAI clearly chose to go broad, opening a wide range of ChatGPT plugins in months. Unfortunately, many of these integrations lack the tight product coupling needed to make them useful. The user experience feels disjointed. This isn’t a new problem. I’ve seen the pitfalls of “breadth over depth” play out before, across various partnership bets in tech. In fact, five firsthand partnership anecdotes from my career illustrate why shallow integrations underwhelm, and why deep, end-to-end integrations are what truly drives the best experience for the customer. Each story, from ride-hailing to meal kits, carries a lesson that OpenAI (or other platforms) would do well to heed.

Today’s post looks at Duolingo — a DTC ed-tech brand with a massive global user base and a freemium model that’s become the standard for language learning apps. The stock has pulled back roughly 65% from its $545 peak this past May, and while this isn’t an investment breakdown, it’s obvious that the market now values one thing above almost everything else: Duolingo’s AI engine and how it scales.

I see two product-led partnership opportunities that could help accelerate that engine:

- A WhatsApp integration that brings Duolingo’s AI Roleplay experience directly into the world’s most-used messaging app

- a fintech-driven rewards program with platforms like PayPal or Revolut to improve LTV/CAC by incentivizing consistent learning behavior.

The WhatsApp idea is the core focus here. The concept is simple: enable language learners to practice short, AI-powered conversations inside WhatsApp — where people already spend a significant portion of their daily screen time. This turns messaging into micro-practice, strengthens daily engagement, and meaningfully improves the value of their emerald customers in Duolingo Max.

Given Duolingo’s scale and WhatsApp’s dominance in markets like India and Brazil (~1B combined users), an initiative like this could drive engagement for ~20M learners and potentially generate $25–30M in incremental annual bookings through Max upgrades.

If Meta platform access, data restrictions, or the OpenAI agreement make that difficult, the fintech rewards angle offers a lighter-weight alternative that still deepens habit formation.

Both directions support Duolingo’s broader mission: make learning “fun and universally accessible,” increase daily engagement, and build differentiated, durable product experiences through partnerships.

Every brand, from a scrappy startup to a Fortune 500, faces the same fundamental problem: How do you get discovered in a sea of consumer choices?

For decades, the answers shifted: first it was getting shelf space at brick and mortar retailers, then Amazon search as online sales took off around 2010. Then Google SEO. In every era, the challenge was the same — being visible in a world where gatekeepers decide who gets surfaced and who gets ignored. Now, the gatekeepers are AI agents.

AI is moving fast, but the business models behind it are even harder to decode. I’ve been spending time mapping out who the key customers are and how money flows through the system. Foundational providers (OpenAI, Anthropic, etc), wrappers (Harvey, Jasper, etc) — each plays a different role in the value chain, and investors and operators alike are still figuring out how to navigate the commercial landscape.

I’ve built and scaled growth models at companies like Newell Brands, Casper, Blue Apron, and Lime, and today I advise startups, investors, and corporates on how to navigate this shifting landscape. To cut through the noise, I created this AI Business Model Guide — a simple framework to understand where opportunities lie and where risks emerge.

If you’re building in AI or exploring partnerships, this guide is a starting point. The presentation is embedded below.

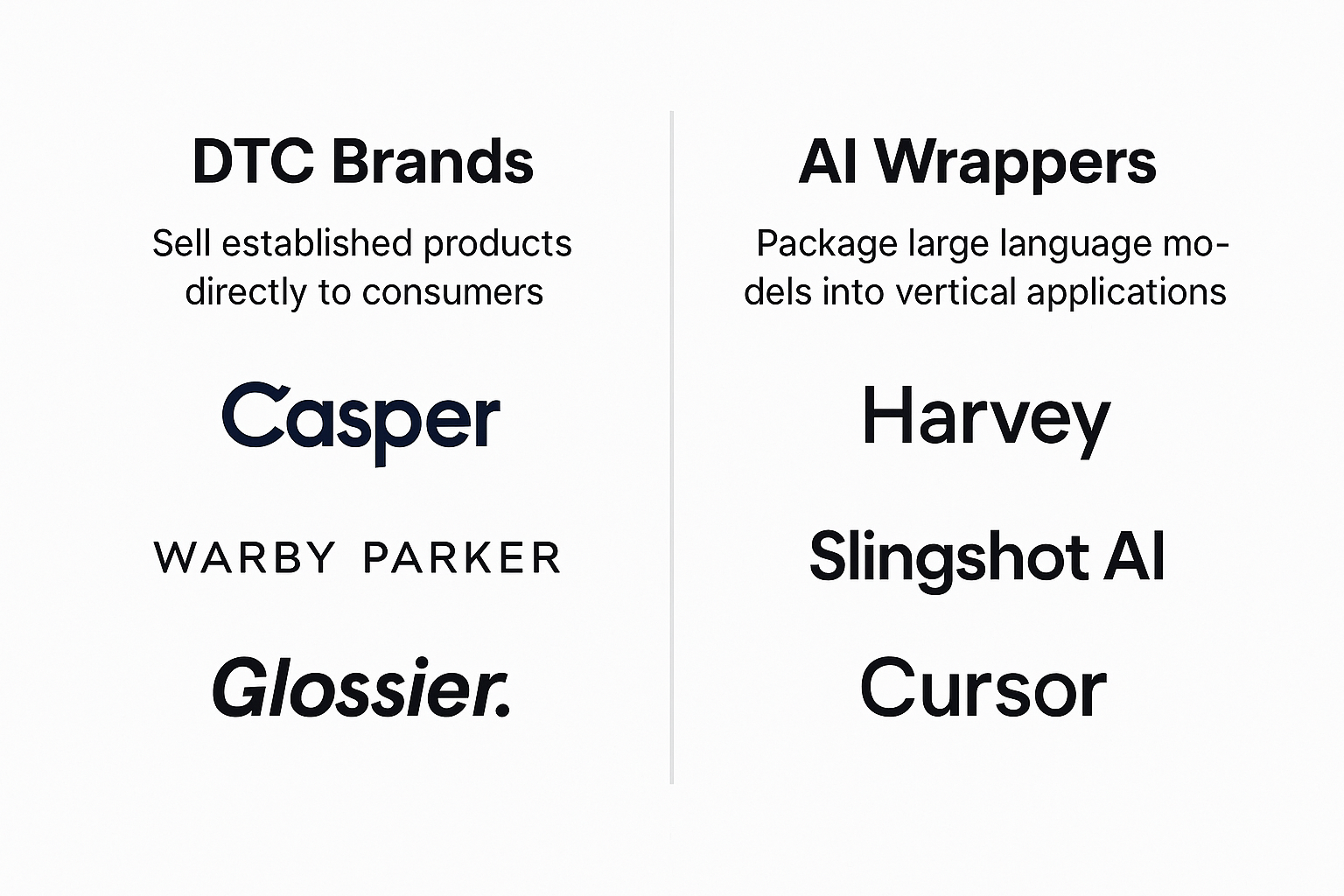

Over the last year, niche AI startups have exploded onto the scene. Companies like Slingshot (mental health), Harvey (legal), and Jasper (marketing), Cursor (code editor) are racing to stake out territory on top of large language models like ChatGPT and Gemini. At first glance, they feel innovative and differentiated. But if you squint, they look a lot like the early wave of direct-to-consumer (DTC) brands — Casper, Warby Parker, Glossier, Harry’s and Peloton — that disrupted incumbents not by reinventing the product, but by reshaping the story, distribution, and consumer experience.

I saw this firsthand at Casper. We weren’t reinventing the mattress — foam was foam — but we were reinventing the consumer experience and telling a story incumbents weren’t telling. We addressed a lot of the pain points in the legacy purchase experience (returns, trial, etc) with novel solutions.

The analogy here is hard to ignore.

The big management consulting firms will have to adapt quickly to AI. The days of paying half a million dollars for a strategy deck are over. By way of example, I was curious, what is next for the food delivery sector (e.g. UberEats, DoorDash, etc) so I put together a prompt and leveraged ChatGPT.

Back in March 2023, I wrote this article about how I was beginning to leverage AI (specifically ChatGPT) in helping me frame business partnerships. This was relatively early in the commercialization of AI. That now feels like an eternity as the space continues to evolve. Today’s post is not an overview of AI – for newbies I highly recommend LinkedIn Learning’s Generative AI for Business Leaders course taught by Tomer Cohen. Google also has a training module on Coursera for business leaders which is a good primer. It’s easy to go down a rabbit hole trying to wrap your head around the space so my recommendation is to start with the basics and then tailor the learning to your specific field.

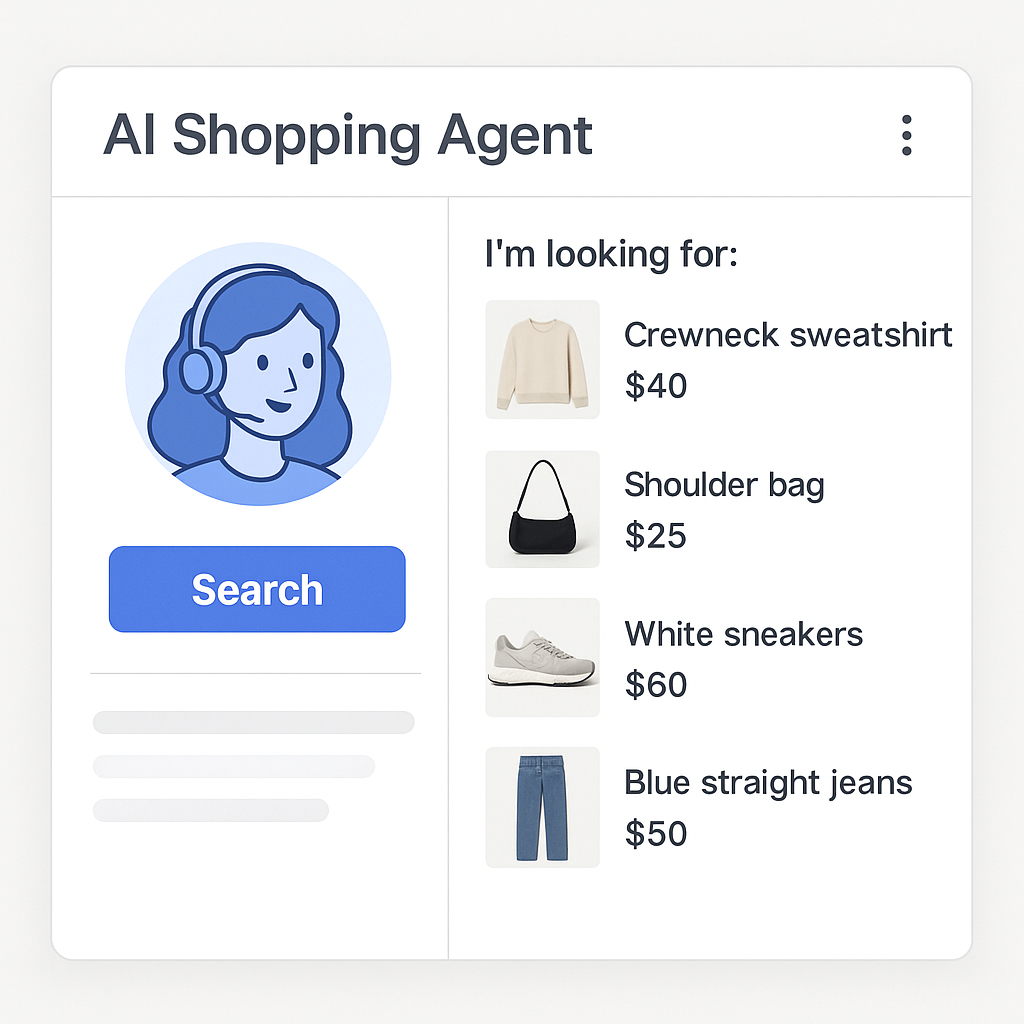

I wanted to share today another use case that has been generating noise and is relevant to retailers and brand marketers – and top of mind for me given my background working in and consulting DTC brands, consumer goods companies, and retailers – the rise of AI shopping agents.

I’ve taken a bit of time off from blogging recently to focus on other things, but recently came across this article from the WSJ about the fall of VF Corp ($VFC) and it reminded me of other legacy brand aggregators, such as Newell Brands ($NWL), that have also struggled as of late. There is a common strategy across both companies – they chose to concentrate key decisions around marketing, product development, and sales at the corporate versus brand level. And the results clearly show that was a mistake.

One of the most difficult aspects of doing partnerships or business development regardless of industry or sector is clearly understanding why two parties should get “married.” In my experience building numerous JV’s/partnerships, one theme continues to resonate, and that is how do you construct a winning partnership where each side feels as if they have gotten equitable value. Oftentimes, initial discussions tend to be more tactical or acutely focused on a very specific asset that one side seeks access to, when the focus should be framing the outcome from inception. This entails being able to articulate clearly the ‘gives’ and ‘gets’ of a deal and not jumping right into the weeds. Jeff Bezos has said, at Amazon, before any work is done on a new partnership, the press release is written. This accomplishes a couple key things.