If you have a small but growing business selling on Amazon or even direct-to-consumer (D2C) you’re bound to hit a point where you require money to scale. For as much as the media talks about venture capital, the reality is that less than 1% of startups here in the US are able to raise money from VC’s. The challenge, however, is that consumer brands often have working capital needs associated with carrying inventory or affording increasingly expensive paid media. So where do these types of businesses get the cash to grow? Traditional lenders, such as banks, often have strict covenants in their terms and have not historically catered their products to this cohort, but a growing number of new, innovative solutions are disrupting the model. I should note that pre-revenue/pre-product startups are likely not going to be a candidate for institutional debt – but a convertible note, SAFE or crowdfunding remain a viable alternative at this early stage. As a side note on crowdfunding, the SEC recently increased the cap for fundraising via this channel to $5m (from $1m) which I suspect will open up more activity in this space.

Venture Debt:

Lenders like Hercules and SVB (Silicon Valley Bank) have a long history in this space and focus on all types of companies in the tech arena. They are typically analogous to a traditional bank but are more flexible and less regulated. Their sweet spot is transaction sizes between $5mm-$200mm. This is a good product for those who need runway extension, IP acquisition financing, corporate expansion and management buyouts. Additionally, they are able to provide asset based financing for equipment or inventory.

Revenue Based Investing (RBI):

Starting a consumer brand today is easier than ever with the proliferation of cloud based tools and SaaS services available (Shopify, etc), but the same can’t be said for growing it.

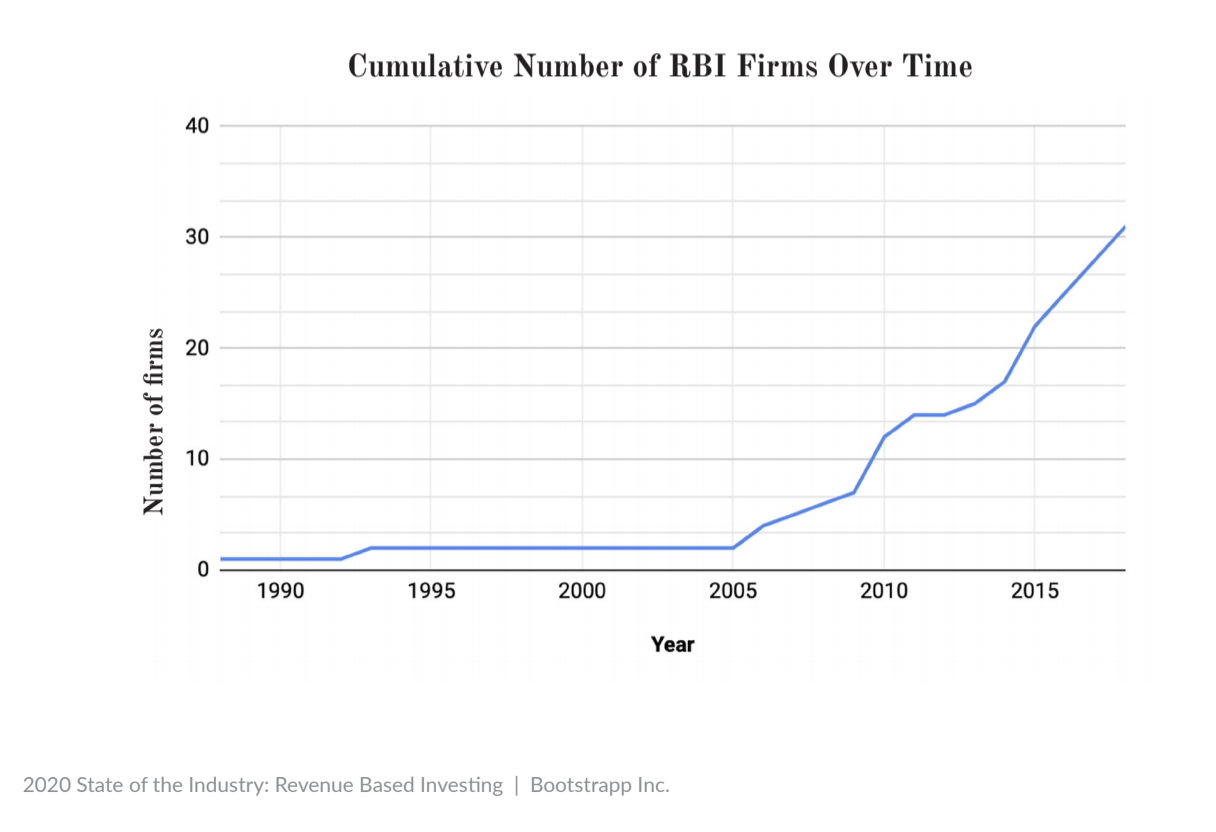

B2C companies require a significant amount of awareness which doesn’t come cheap. Startups that have raised venture capital in this space are essentially using that cash to subsidize marketing which is an, arguably, poor use of that capital. Why dilute yourself now, when you can use alternative methods like revenue based financing to get traction, scale and then raise VC dollars at a higher valuation. A large swath of revenue based financing partners have come to market over the last 4-5 years and honed in on D2C startups and Amazon 3rd party sellers. (Chart below)

Some to check out include Upper90, Clearbanc and Liquidity Capital and PIPE. Additionally, even the payment processor Stripe is getting in the game of lending to startups. If you currently use Stripe as your payment gateway, you should consider learning more about their other products. You’re in the sweet spot to take advantage of this model if your business shares these traits:

- Recurring Revenue – lenders like to see historical patterns of repeat purchase

- Profitable or path to profitability

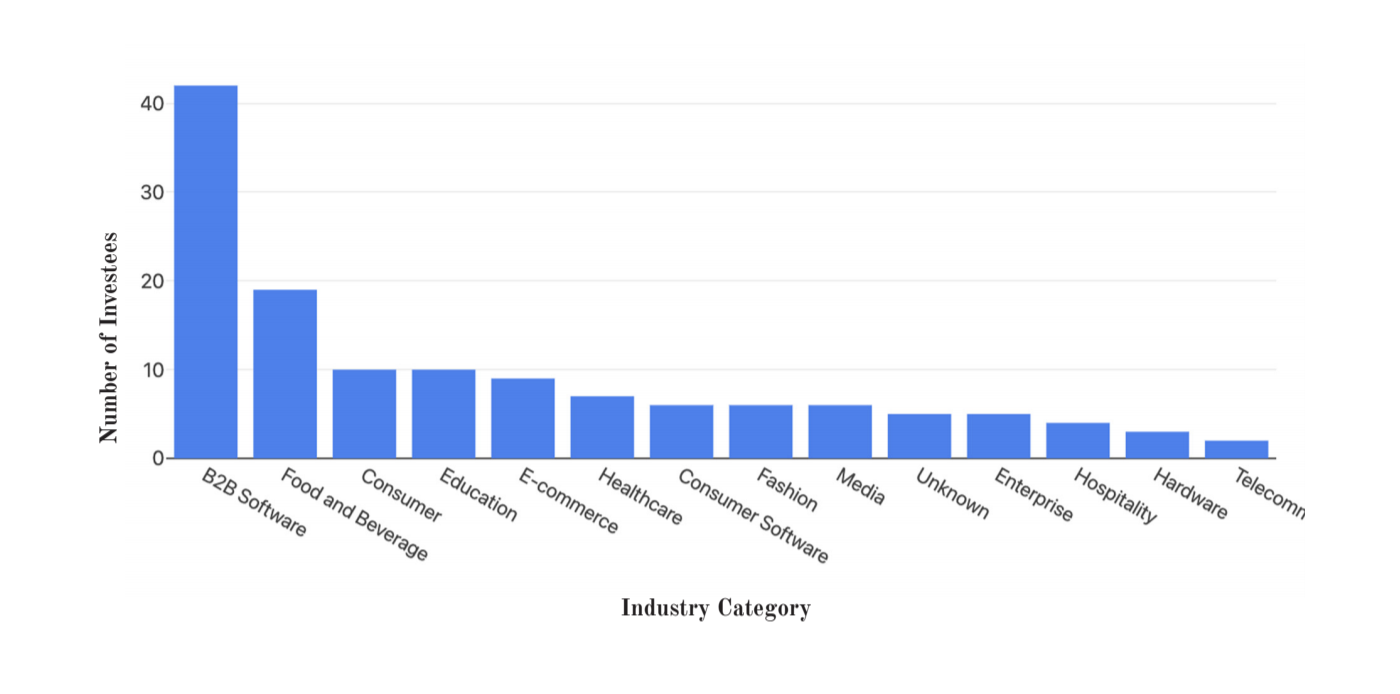

- B2B SaaS – startups in this space typically have customer contracts that demonstrate predictable revenue and can be securitized.

- D2C – Food and beverage (F&B) and other consumer staples also are ripe for this type of investment.

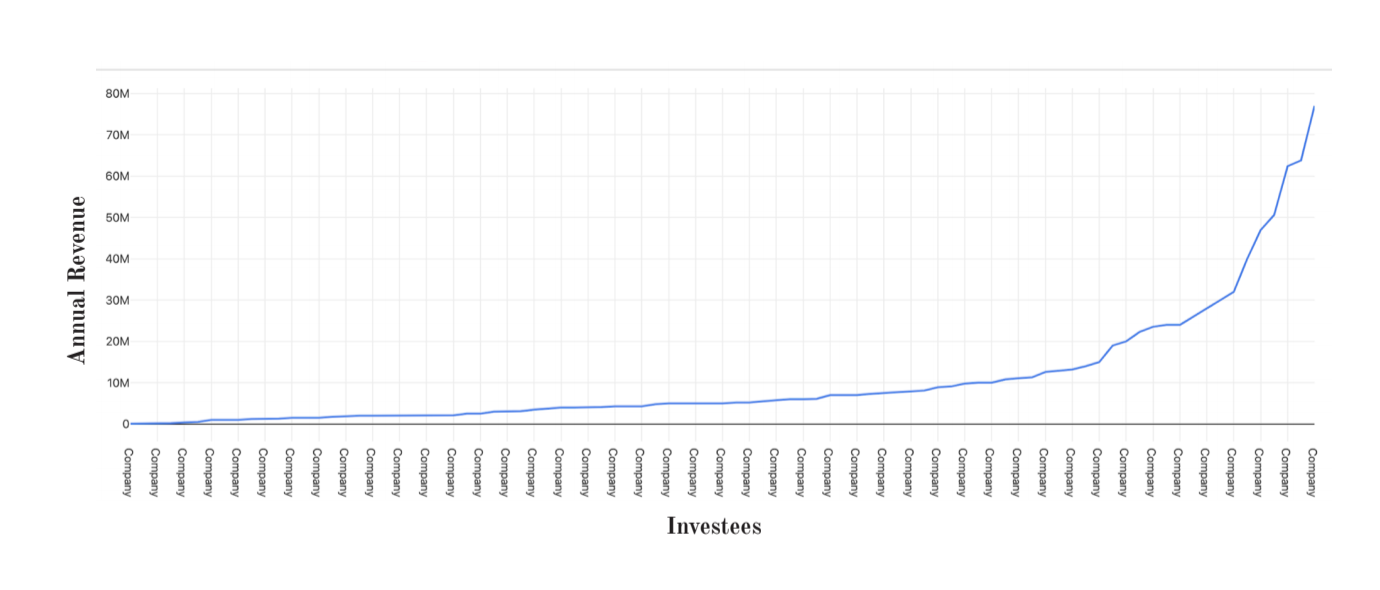

- Annual revenue of $3m+ (the vast majority of companies generate <$20m in annual sales according to Bootstrapp)

As it pertains to repayment, the model works whereby the startup repays the principal plus a fee to the lender out of future revenue with the typical percentage ranging from 3-8% monthly. Some agreements include a repayment cap – often expressed as a multiple of the principal (e.g. 1.5x, 2x, 3x). Lastly, you’ll see some agreements even add warrants and other conversion-to -equity triggers. I’m not a fan of this as it can further muddy the cap table if you plan to take institutional capital via equity in the future. RBI isn’t for everyone, but the cost of capital should be weighed against other avenues as you’re looking to scale.

For companies that generate recurring revenue from subscriptions, PIPE can provide upfront capital without debt or dilution. PIPE takes those subscription contracts and sells them to other investors (turning them into tradable securities effectively).

Lastly, for those who have a business selling primarily on Amazon’s marketplace, Yardline is a lender who can not only provide growth capital but also has significant experience with the intricacies of selling through this channel. An added benefit, they are backed by Thrasio (the largest acquirer of Amazon brands) which can set up a nice pathway to a potential exit.

While debt is surely not without risk and ideal for everyone, there are some benefits. The primary feature is that you often don’t have to give away much equity (if any) meaning you can retain more control of your company. When Microsoft went public, Bill Gates owned 49% of the business, whereas the average founder now owns <15% at an IPO – a result of companies staying private longer.

I love seeing innovation in sources of capital for startups and hope other models continue to emerge.