As I was reading last week about how McKinsey was hired to help Disney streamline costs this year, it drew similarities to my time at Jarden when we merged with Newell in 2016. MK is a great firm, don’t get me wrong, but I continue to see this playbook applied that doesn’t always work. Centralization is not invariably the answer, especially in businesses with strong IP and nuanced relationships.

Given what was ultimately mostly a Disney+ profitability issue in my opinion, MK recommended centralizing all content decisions/spending in a newly formed corporate group, thereby taking away power from the studios and content creators who had previously managed their own budgets and were closer to the end consumer. That’s a drastic move to make when the underlying issue lives mostly within just one segment of a large empire and ultimately related more to pricing of the product and customer acquisition cost, but I digress. After a year in which Disney stock has declined 40%, Bob Iger, who previously ran the company, was brought back in to fix things – task number 1, disbanding this centralized approach to content spending.

In 2016, while I was at Jarden, the company was acquired by Newell Rubbermaid. Jarden’s stock was at a near all time-high – but Newell’s management thought they could accelerate it further via a slew of synergies. On the surface the companies looked somewhat similar – both sold household products primarily through wholesale, both sourced from similar factories in Asia and the two shared a lot of customer demographic overlap. But there was something fundamentally different between the two organizations. Newell preferred to centralize a lot of key choices around innovation, sales, and e-commerce, why Jarden operated more similarly to a holding company – with each business having a large amount of autonomy to make decisions and take risks.

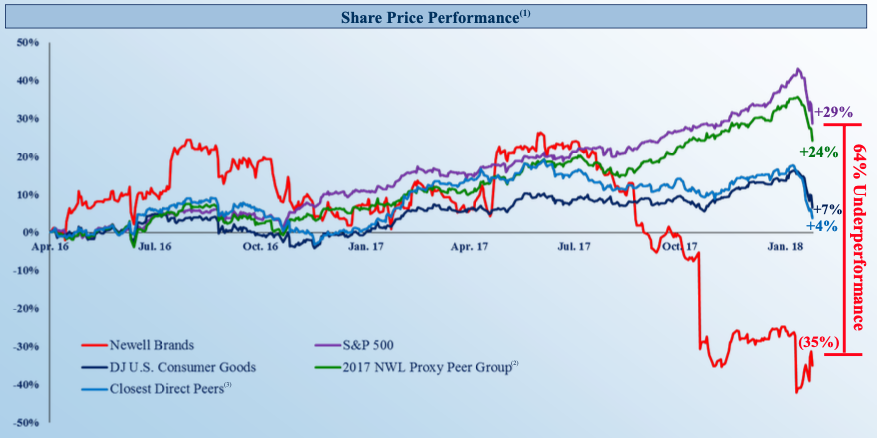

After the deal closed, Newell hired two large management consulting firms to mold Jarden into its operating model. The results were underwhelming as you can see in the chart below. Within two years of the deal closing, Newell’s stock had significantly underperformed vs its peers.

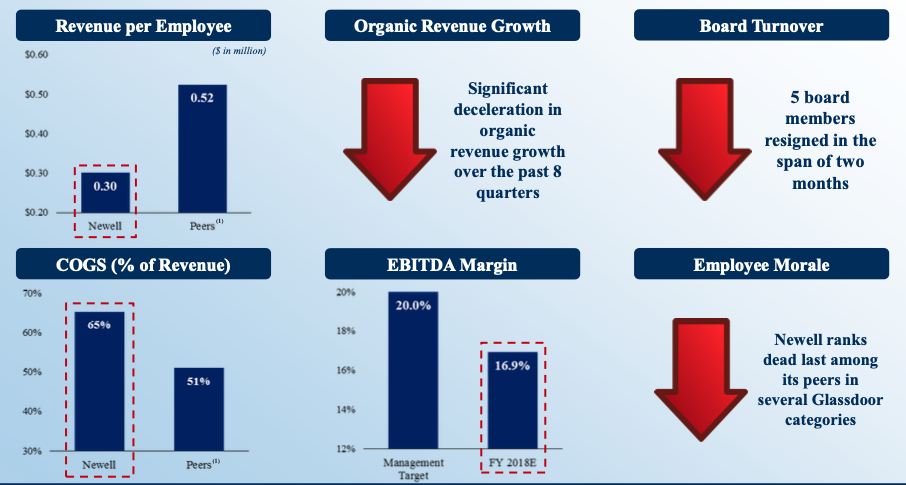

And under the hood, many core KPI’s such as COGS and EBITDA were struggling.

So, what ultimately was the reason for this drastic underperformance vs peers? The answer is it was self-inflicted and not a sign of larger macro issues.

The most cogent argument I believe is that Newell was building products that retailers and customers didn’t want. Under the Jarden model, each business unit performed separate R&D and worked closely with retailers to design products that customers desired. While, under the Newell model, innovation was centralized and often misaligned with customer needs. Furthermore, marketing was also centralized, and spending was controlled by a group that didn’t understand a lot of the cultural nuances of the various owned brands. For example, Newell deciding to stop sponsoring pro athletes on the K2 or Marmot brands because the centralized team didn’t have experience here had devastating consequences for awareness and relevance. Drawing parallels to the Disney example, centralizing content decisions caused the company to misjudge what viewers wanted and alienated the creative teams who had previously had their own marketing budgets. This caused dislocations in the industry as a team was applying a one-size fits all approach to a wide swath of content. This led to a lot of film and TV IP that turned out to be duds or were not marketed to the right audience – which ultimately put pressure on margins.

Disney is nothing without its IP the same way that many of Jarden’s legacy brands like Marmot, Coleman and K2 would not have been successful without the outdoor sports trade vertical. Different industry, but very similar lesson – centralization comes with risk that often consulting firms have a hard time distinguishing.