When I was at Jarden (now Newell Brands), we always had clear acquisition criteria when it came to M&A.

- Strong cash flow characteristics

- Category leading positions in niche markets

- Products that generate recurring revenue

- Attractive historical margins / or margin expansion opportunities

- Accretive to earnings

- Post earnout EBITDA multiple of 6-8x

This strategy allowed us to grow from one brand (The Ball Jar company in 2002) to over 50 brands and ~$8b in sales by 2015 when the company merged with Newell Rubbermaid.

This model represented the classic rollup strategy. These acquired brands we brought into the fold typically had strong awareness and deeply entrenched wholesale relationships in addition to being primarily majority owned by PE firms. The low hanging fruit was being able to extract economies of scale from the combination. But this model was far from perfect. There was a ton of bloat and market nuances in these acquired brands that were sometimes difficult to remove. The idea was by having multiple brands, you could gain more favorable placement/economics at the large big box retailers. Ultimately, as we found numerous times, while this did help improve unit economics slightly, there were ultimately, newer, digital-first brands waiting in the wings to take our position. Additionally, sourcing an acquisition target, going through lengthy and expensive due diligence with bankers and lawyers – all led to closings that took months. And speed is crucial in consumer brands where trends can change quickly.

This leads me to question, what if there is now a better way for CPG’s and the like to build a leaner, quicker rollup strategy – one that provides easier discovery, a better acquisition multiple, an e-commerce beachhead and is overall more expeditious.

There’s a growing number of startups that are creating the framework for the new rollup model of the future and where else better to get potential targets than Amazon.

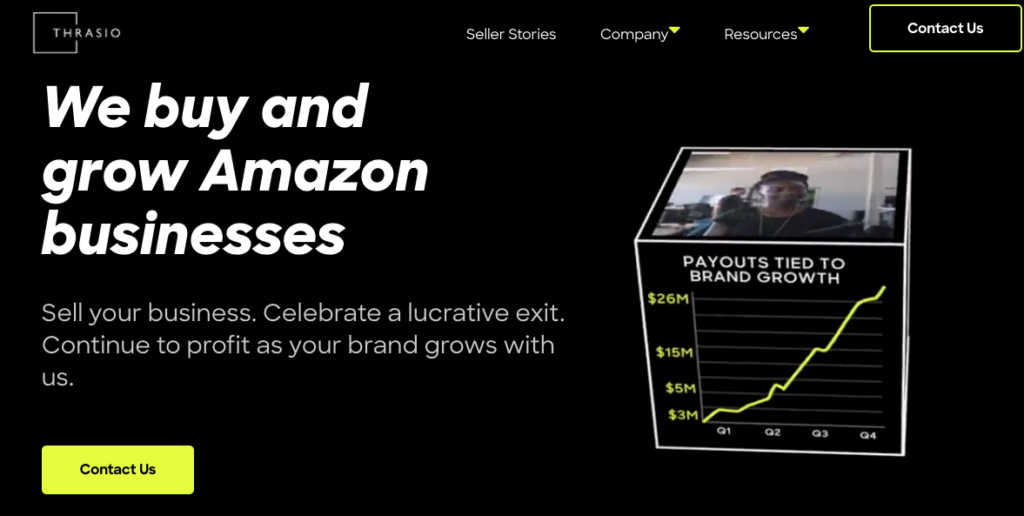

Here’s an example of how one of the largest, Thrasio works:

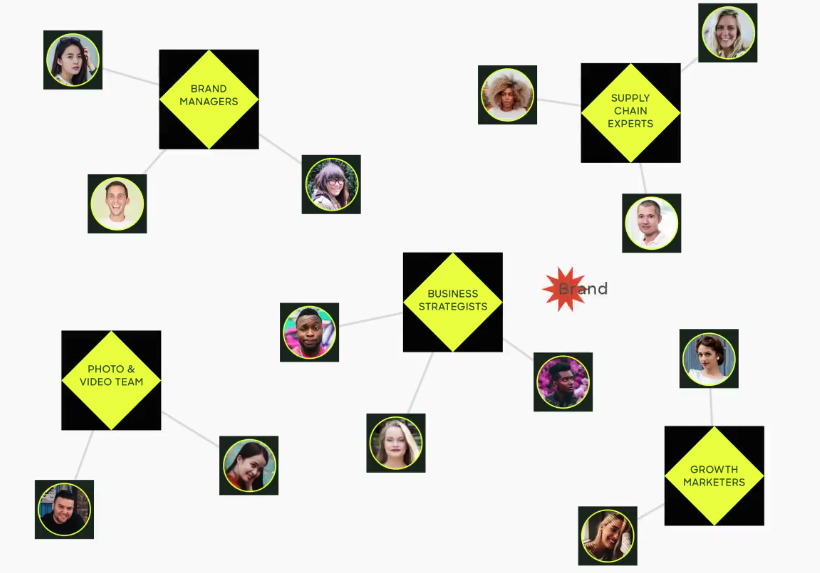

Thrasio looks for typically smaller-family run businesses selling on Amazon with 1-2 products that are top sellers in their respective categories and doing between $1m-$5m/arr. Note: However, given additional capital raised, they now are looking for brands up to $200m/arr – opening up an even larger part of the market. They offer to acquire the brand from the entrepreneur for a post earn-out EBITDA of 6x and typically close in <35 days. They then leverage back office functions to gain efficiency in these key areas:

- Supply Chain – they negotiate more favorable ocean freight costs by using their scale of acquired brands. Since contribution margins typically are constrained as more products are rolled out Thrasio can get efficiencies from consolidating suppliers, etc.

- Marketing/Collateral – they can get reduced advertising rates by participating in upfront deals with media companies. Furthermore, they can share in-house marketing service functions that specialize in photography, etc to lower total cost. Selling online requires a significant number of digital assets and most smaller companies don’t have the resources to develop these in-house.

- Merchandising – they are able to cross-sell: bundle, up-sell, offer GWP’s, rebates, etc

- Offline Retail/Wholesale – they can get better leverage with retailers when selling in their suite of products given scale. The same way we often sold CrockPot and Oster into the buyers at Walmart to gain more favorable placement on shelf and deal economics, Thrasio is able to do the same.

- Data – There are a multitude of data efficiencies that come with scale. Example: Imagine they purchase a baby care brand and can now market other products for mom’s in their portfolio.

Compare this with a classic CPG that doesn’t have the relationships or model to find fast growing brands from Amazon or other e-commerce platforms. Their default source for M&A has been through legacy channels like PE or even Venture Capital (where they are likely overpaying) in many cases. Complicating matters further, over the past few years there’s been increasing antitrust concerns that have dampened interest among large CPG’s to consummate deals that could trigger FTC intervention (Harry’s and Billie, for example). Furthermore, these brands likely have peaked or are hitting their prime. Because these deals aren’t typically tuck-in acquisitions, management often needs board approval which can drag out the entire process and be a distraction for the management team that needs to execute. Post purchase, integration is often fraught with issues as well – large CPG’s have good intentions when they make acquisitions to extract value but I can tell you firsthand that individual business units aren’t often structured or incentivized to realize this. During the Newell/Jarden tie-up, I was a member of the Transformation team focused on trying to ascertain $500m in synergies that were promised to the street. No amount of money spent on expensive management consultants could fix the fact that procurement exercises don’t often yield what we expect. All this leads to an incredibly high failure rate – 80-90% of M&A fails to deliver value (HBR).

Meanwhile, Thrasio, which has acquired well over 100 brands, claims the EBITDA of its targets has increased 156% post purchase.

This is all to say that the CPG rollup model is being reinvented with a digital first lens and corporate’s should take notice.

Here are some ideas of how the aggregators can continue building capabilities:

- Licensing

- These companies should develop an asset light licensing expertise to line extend some of their most promising brands into new categories.

- M&A as a Service

- The way many VC as a Service funds are popping up, the aggregators should consider outsourcing some of their M&A engine to corporate’s who are looking to acquire brands more efficiently but lack the relationships. Furthermore, they eventually will be in a position where they need to jettison brands and this network of corporate’s could be the best buyers.

- Wholesale/B2B

- While most of the aggregators are focused almost exclusively on Amazon brands today, they obviously won’t be married to this platform for potential deals indefinitely. E-Commerce still only represents ~15-20% of total US retail sales which means that in order to grow they’ll inevitably have to build a robust wholesale business selling into big box retailers and the like.

- Services

- Services are a high margin complement to a product based business as I’ve talked about here. Extended warranties and other digital solutions should slowly be merchandised.

- Incubator

- With all the data intelligence they are capturing on consumer behavior, it’s possible that they are able to harness all of this data to create their own brands, spin up private label or even white label for others.

- Alternative funding

- Not every entrepreneur is looking to sell, but most need cash to grow. Offering debt via revenue based investing and other channels is a good way to build a relationship and deal pipeline to eventually set up for an acquisition. This is one of the reasons that Thrasio purchased Yardline Capital – to offer other capital solutions.

- Owning a Category

- I mostly see the aggregators be somewhat agnostic to category – but the reality is eventually this needs to be prioritized. Are you building a next generation Williams Sonoma (Pottery Barn, West Elm, etc) or the future VF Corp in sporting goods – having a hodgepodge of brands, while it may work now, ultimately will be very difficult to extract real synergies. At Jarden we divided our company into three branches – Kitchen Products, Outdoor Sporting Equipment and Branded Consumables. When we merged with Newell Rubbermaid in 2016, it became clear that many brands didn’t fit into a defined bucket and ultimately these were slowly sold off post combination. Why is this important? For example, at Jarden, our sporting goods business performed best in Q2/Q3 and our kitchen products did best in Q4/Q1 – this provided a nice anchor to the company and helped offset any weakness in other parts of the year. Most brands sold on Amazon that the aggregators are purchasing are easily replicable – ultimately offering low margin and little product differentiation. Even large CPG’s like Unilever realize that growth is going to come from emerging categories like heath and beauty and are jettisoning brands in other areas. If the large incumbents (i.e. Unilever, P&G, Nestle, etc) are rotating, this should be a harbinger for the aggregators to follow suit.