I continue to see the surplus of food delivery companies and F&B marketplaces on an impending crash course. Is DoorDash a retailer, a logistics company, a brand, a restaurant or even a media/data company? Their vision is likely to be a bit of each and this will be accomplished under a build, partner, buy framework. Like numerous other industries, the idea of a horizontal play has turned vertical and we’re starting to see each encroach the other’s territory. The challenge in the future will be how to become the super app that customers interact with daily. This fight for share is not without challenges. The average smartphone user has 80 apps on their phone, but they only use ~9 apps per day and 30 apps per month. This means that 62% of those apps don’t get used much, if at all.

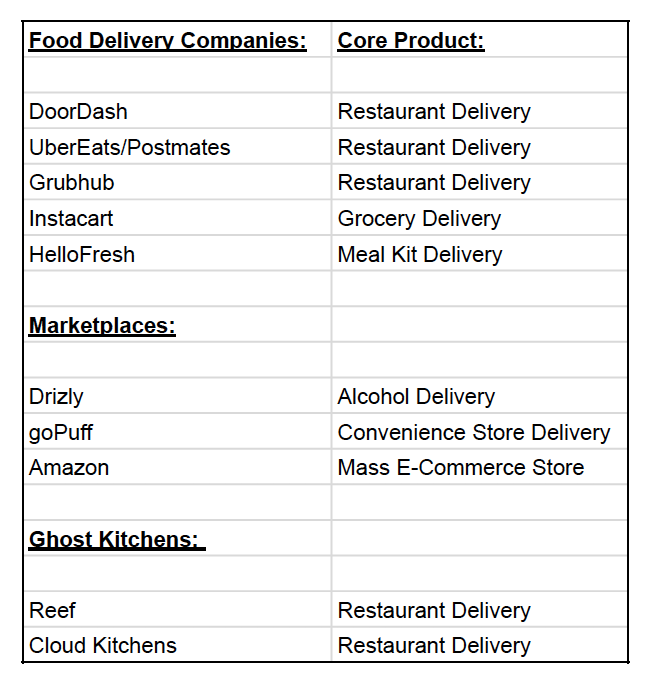

Here’s a list of the key companies that make up this space along with their core product:

Competitive Position:

Using DoorDash as an example of how this space is converging let’s look at three key areas: Control of last mile, Connecting with physical retail and lastly sourcing directly from brands/manufacturers (see chart)

1.0: DoorDash began as an app connecting consumers to restaurants for meal delivery

2.0: App connecting consumers to retailers (not just restaurants) as an alternative point of distribution. If BestBuy wants to have a TV delivered in an hour, they’ve historically not been able given their supply chain. Now DoorDash can provide this service.

3.0: App connecting consumers to brands directly as a new point of distribution. Keeping the electronics analogy, if Samsung wanted to get a new television to a customer in an hour, DoorDash could go to Samsung’s DC’s, pick it up and deliver it – circumventing BestBuy altogether. And because many brands have spent the last 5+ years heavily building up their own D2C operation they have the infrastructure in place to support this.

4.0: DoorDash creates a media division that allows merchants to get preferred positioning on the app (think Amazon’s AMG group) – and also sells consumer data to the large CPG customers. For example, DoorDash coud report to Pepsi-co that people often buy Pepsi with Doritos on a specific day and time during the week which would help the large CPG better tailor product mix, bundling and even aid in potential product development. Presently, Pepsi get’s very limited qualitative data from their existing wholesale accounts but DoorDash, by nature of their model, can ascertain this more efficiently.

Long term questions/opportunities: Does DoorDash start holding inventory (significant cap ex cost, warehousing, etc or do they open a 3rd party marketplace (ala, Amazon). Do they bundle fintech solutions and offer financing to customers directly? This is another high margin service product with high attachment especially on larger ticket items like TV’s. Lastly, does DoorDash white label their tech for other parties – essentially creating a super logistics juggernaut that would allow expansion into adjacent fields with less capital at risk.

Based on their S1, you can begin to see this evolution; they ultimately believe there is value in controlling all aspects of the customer experience as well as merchandising.

While DoorDash and the other food delivery companies are likely to continue to verticalize their product offerings, a marketplace like Drizly is likely to be headed in the same direction.

Today Drizly offers alcohol delivery in <60 minutes. They don’t hold inventory or do delivery (Update: Feb 21: Uber acquired Drizly – once again showing how this industry is moving vertical). Their app connects brick and mortar merchants directly with customers. The challenge/opportunity?

- Customer Experience – Drizly doesn’t actually deliver anything, instead relying on their merchants to handle this task. Considering a key part of their value prop is quick delivery, there’s a critical piece of the business that they don’t ultimately control. It’s incumbent upon the merchant to fulfill delivery. This isn’t often a retailer’s core competency, so this often gets outsourced to folks like DoorDash. So while DoorDash has a great 2nd removed partner in Drizly, they also recognize that they could have brokered this transaction directly (model 2.0 above).

- Work directly with the manufacturer (ex. Diageo) vs. just working with the local liquor stores – further building commercial partnerships and accessing potentially better unit economics. Secondly, these brands are constantly looking for new consumer insights to aid in product development. Drizly could help identify key trends around alcohol consumption at a specific moment in time. For example, Drizly published key learnings on what beverages consumers chose to drink most this past New Years Eve. This level of data is harder for a big brand to ascertain from retailers who often can take weeks to deliver quantifiable insights – if they even choose to at all.

Lastly, the Cloud Kitchens operators are also looking to verticalize. Today, they are focused on building central kitchens that do nothing but prepare restaurant style meals that are then delivered to customers by the delivery companies. What’s potentially next?

M&A/Franchising: eventually one of the large delivery networks likely acquires/merges with a cloud kitchen company giving full control over the customer experience. Furthermore, companies in this space, like Reef, will see an arbitrage opportunity to broker franchise fees/licensing revenue on behalf of their Ghost Kitchen tenants. Taking this one step further, Reef could also do a rollup through M&A and build out a massive food holdco (think what Thrasio is doing with independent sellers on Amazon). In the end, I could imagine a world in which Reef is not only a real estate investment company but also owns hundreds of restaurant concepts. Using an example from another industry, Simon (the large mall operator) has slowly been buying up brands that used to be tenants in their malls – another example of vertical growth.

What does this all mean?

There has to be consolidation. We’ve started to see some horizontal M&A focused on the delivery piece, (Uber & Postmates and now Uber expanding to the marketplaces directly via the Drizly acquisition) but in the next couple of years more tie-ups are on the horizon especially in other areas of the value chain. Consumers don’t have an interest in having multiple apps that essentially deliver very similar services. In China, this dynamic has led to a few super apps like WeChat that provide everything from delivery to banking, etc. Barring any antitrust concerns (which is a real possibility), we’ll likely end up with the same model here.